South Africa’s auto manufacturing sector is at a crossroads. It contributes 5.3% to GDP, supports 500,000 jobs, and relies heavily on exports, with 45% of vehicles shipped to the EU and UK – markets that plan to ban internal combustion engines by 2035. Despite its size, the industry faces serious challenges that threaten its future:

- Low-cost imports: Chinese and Indian brands dominate, with imports making up 69.3% of light vehicle sales by 2025. This has led to factory closures and job losses.

- Infrastructure issues: Inefficient ports, unreliable rail services, and power outages disrupt production and exports.

- Lagging local content: Local content levels dropped to 38% in 2023, far from the government’s 60% target.

- Global EV transition: South Africa risks losing key export markets unless it shifts to electric and hydrogen vehicles.

To address these challenges, the government is introducing tax breaks, higher import duties, and incentives for electric vehicle (EV) production. For example, a 150% tax deduction for EV investments starts in March 2026. Manufacturers like BMW and Ford are already committing to hybrid and EV production locally.

The industry’s future depends on tackling infrastructure issues, increasing local content, and transitioning from semi-knocked-down (SKD) to completely knocked-down (CKD) production. CKD creates more jobs and aligns with long-term growth goals. South Africa’s rich mineral reserves also position it as a potential leader in EV battery production, offering new opportunities for growth.

South Africa Auto Industry: Key Stats, Challenges & Opportunities 2025

Current State of South Africa’s Auto Assembly Sector

Production Volumes and Employment

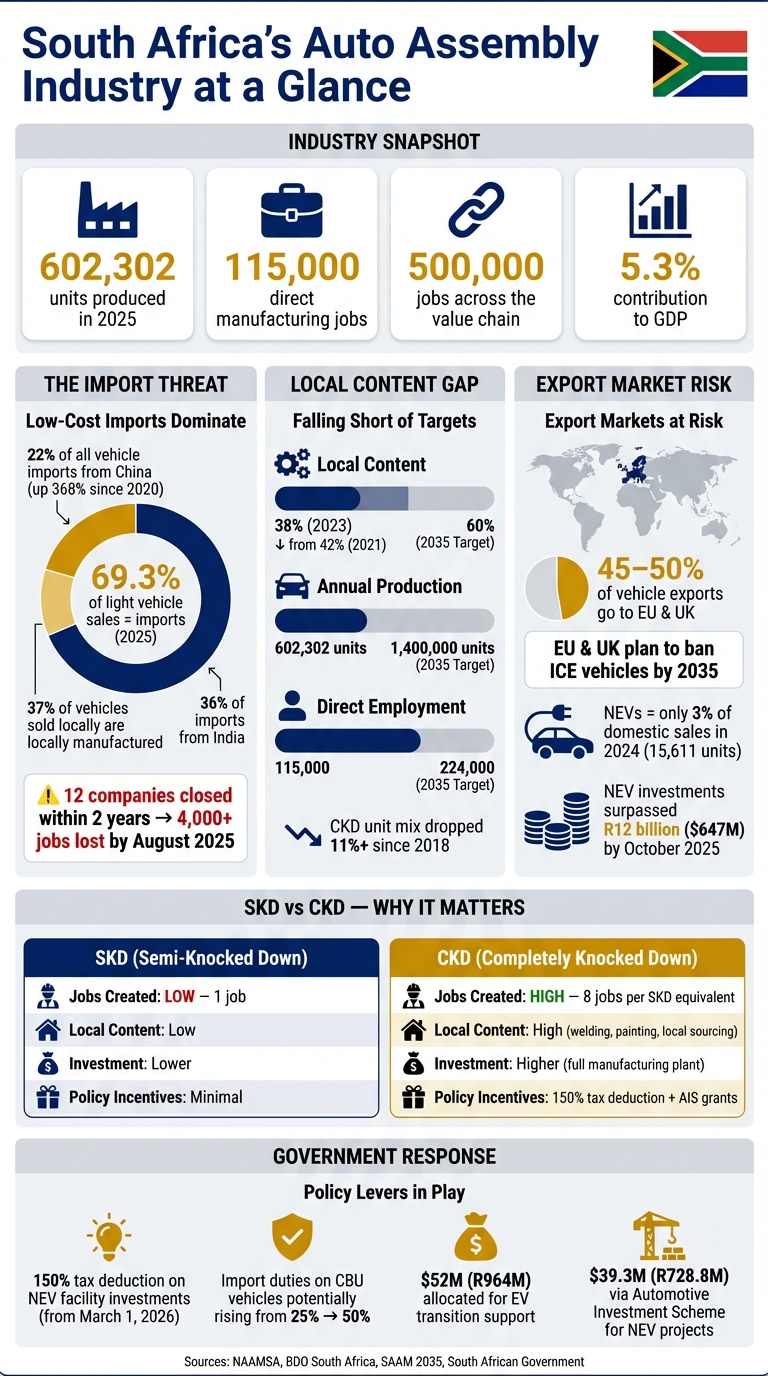

In 2025, South Africa’s auto assembly sector produced 602,302 units, maintaining its position as the country’s largest manufacturing industry. The sector directly employs over 115,000 people and supports an additional 500,000 jobs throughout the broader automotive value chain. President Cyril Ramaphosa highlighted its importance, stating:

"The sector currently supports more than 115,000 direct manufacturing jobs and more than 500,000 across the value chain. It contributes approximately 5.3% to GDP."

Despite its scale, the industry is grappling with serious challenges. Infrastructure issues at ports, inefficiencies in rail transport, and a new 30% export tariff imposed by the United States have created significant operational hurdles [9,15]. Compounding these issues, localization efforts have faltered, with local content levels dropping from 42% in 2021 to just 38% in 2023 – far from the government’s 60% target. The reliance on imported components is becoming more pronounced, as reflected in the decline of Completely Knocked Down (CKD) unit production. CKD units, which involve local assembly of imported parts, saw a sharp drop of over 11%, from 54% in 2018 to 60% in 2023. Siyabonga Mthembu, Automotive Sector Leader at BDO South Africa, commented:

"SA’s Completely Knocked Down (CKD) unit mix has deteriorated by more than 11% since 2018… constituting of more being imported rather than produced locally."

These challenges are further exacerbated by increasing competition from imports.

Impact of Import Competition

Adding to the internal pressures, South Africa’s auto sector is contending with a flood of low-cost imports, which have reshaped the market landscape. By 2025, imports accounted for a staggering 69.3% of light vehicle sales, leaving local manufacturers struggling to keep up. Brands from China and India, such as Chery, Haval, and BYD, have aggressively entered the market, particularly in the hybrid and electric vehicle segments, offering attractively priced alternatives.

The fallout has been severe. Within two years, twelve companies ceased operations, resulting in over 4,000 job losses by August 2025. Trade Minister Parks Tau addressed the issue, stating:

"Twelve companies have closed operations within two years, and more than 4,000 workers have lost their jobs."

Notable closures include Goodyear’s tire plant in the Eastern Cape, reduced production at Nissan’s Rosslyn facility, and Ford’s August 2025 layoffs of more than 470 workers across its assembly and engine plants due to shifting demand [9,15,16]. Local executives have also raised concerns about foreign manufacturers engaging in vehicle dumping, aided by large-scale production and government subsidies. David Furlonger, Editor-at-large at Business Day, remarked:

"Some local brands are becoming virtual spectators as these new, low-priced competitors gobble up market share."

These developments highlight the urgent need for policy intervention and a focus on innovation, especially as the industry moves toward electric and alternative energy vehicles.

sbb-itb-09752ea

Challenges Facing South Africa’s Auto Assembly Industry

Infrastructure and Energy Constraints

South Africa’s auto assembly sector is grappling with serious infrastructure and energy challenges. The country’s deteriorating port and rail systems are causing delays in both importing components and exporting vehicles. South Africa’s ports rank among the least efficient globally, leading to significant bottlenecks. On top of that, Transnet-managed rail services are plagued by inefficiencies, forcing manufacturers to use expensive road transport to move vehicles between key production hubs like the Eastern Cape and Gauteng.

Energy reliability is another pressing issue. Frequent power outages and rising electricity costs are disrupting operations just as the industry looks to transition toward electric vehicle (EV) production. Siyabonga Mthembu, Automotive Sector Leader at BDO South Africa, highlighted this concern:

"Eskom must address the issue of the high cost of electricity which could present a significant barrier to widespread EV adoption."

To address these energy challenges, manufacturers are turning to self-generation projects. For example, Mercedes-Benz South Africa has invested $5.4 million (R100 million) in photovoltaic expansions at its East London plant, while BMW has committed $243 million (R4.5 billion) over five years to ready its Rosslyn facility for plug-in hybrid production.

The situation is particularly dire in industrial centers like Nelson Mandela Bay. In October 2025, Deputy Mayor Gary van Niekerk launched a "Project Management Unit" to tackle complaints from manufacturers like Isuzu Trucks SA about failing infrastructure, unreliable water supply, and security risks. Van Niekerk pledged:

"This metro will be the place where the roads are strong, the lights stay on, the water flows, and communities and businesses feel safe."

These operational obstacles are compounded by the industry’s struggle to meet local content and skills development targets.

Skills Shortages and Local Content Goals

Beyond infrastructure woes, South Africa’s auto industry faces difficulties in achieving local content targets and addressing a shortage of skilled labor. The SAAM 2035 targets – 60% local content and 1.4 million annual units – remain distant goals. In 2025, the industry produced just 602,302 units, less than half the target [18,23].

One major hurdle is the underdeveloped local supplier network. Many manufacturers rely on imported components, as subsidized Chinese production offers up to a 30% cost advantage. This reliance on imports has also stalled employment growth, with the sector employing only 115,000 people in 2024 – far short of the 224,000 jobs envisioned by 2035.

The labor shortage is especially acute in artisanal trades like fitters and turners, as well as in specialized EV technologies. Current training programs often fail to align with specific business needs, leaving manufacturers without the skilled workers required to increase local content.

Efforts to bridge these gaps are underway. For instance, in January 2026, the Automotive Industry Transformation Fund (AITF) approved R667.8 million in funding, benefiting 75 projects and creating 2,754 jobs. However, the rigid structure of the Automotive Production and Development Program (APDP) incentives discourages further investment. If employment numbers fall even slightly below the required threshold, manufacturers risk losing their entire incentive payments.

Adding to the complexity is the rise of Semi-Knocked Down (SKD) assembly models. Unlike Completely Knocked Down (CKD) operations, SKD assembly involves minimal local content and generates only one job for every eight created by CKD. Professor Justin Barnes, an automotive policy adviser, criticized this trend, stating:

"To encourage SKD would be massively retrogressive. If the government incentivises SKD, it is supporting a race to the bottom."

Government Policies Shaping the Industry’s Future

Review of the Automotive Production Development Programme (APDP)

The Automotive Production Development Programme (APDP) has undergone a shift in focus. While it previously rewarded production volumes, the program now prioritizes local value creation through the Volume Assembly Localisation Allowance (VALA).

In 2025, the government updated APDP2 to include New Energy Vehicles (NEVs) – electric and hydrogen-powered cars – within its incentive framework. This change aligns with the European Union and United Kingdom’s plans to phase out internal combustion engine vehicles by 2035. These regions represent nearly half of South Africa’s vehicle export market.

Industry leaders are calling for changes to the APDP that would better support completely knocked down (CKD) operations over semi-knocked down (SKD) assembly. CKD plants, like Volkswagen‘s facility in Kariega, generate around eight jobs for every one job created by SKD operations.

The government is also exploring ways to extend the APDP framework to guard against global trade challenges. Parks Tau, Minister of Trade, Industry and Competition, highlighted this during recent discussions:

"What we’re currently considering is the possibility of expanding the automotive industry production plan so that we’re able to mitigate the impact in our industry [of U.S. tariffs]."

In addition to production incentives, the government is introducing targeted tax reforms aimed at strengthening domestic manufacturing.

Tax Reforms and Luxury Vehicle Tariffs

Complementing the APDP updates, new fiscal measures are being introduced to protect the industry and encourage NEV adoption. Starting March 1, 2026, manufacturers will be allowed to deduct 150% of their investments in NEV facilities from taxable income. For example, a $1 million investment in electric vehicle assembly lines could result in a $1.5 million tax deduction.

President Cyril Ramaphosa has also called for incentives aimed at consumers, emphasizing the need for subsidies or tax rebates to boost electric vehicle adoption:

"Consideration must be given to incentives for manufacturers, as well as tax rebates or subsidies for consumers, to accelerate the uptake of electric vehicles."

The government has allocated $52 million (R964 million) over the medium term to support these initiatives.

On the import front, the Department of Trade, Industry and Competition is considering raising duties on completely built-up (CBU) vehicles from the current 25% to as high as 50%. South Africa’s World Trade Organization tariff ceiling for such imports is 50%, leaving room for adjustments. This review comes as Chinese vehicle imports surged by 368% between 2020 and 2024, now making up 22% of all vehicle imports.

However, industry leaders have raised concerns about the potential impact of steep tariff increases. Peter van Binsbergen cautioned:

"Fifty percent would be a shock and we don’t want to shock the system because there’s often unintended consequences… The worst being affordability for an entry-level consumer who has double the duty put on a car."

Deputy Minister Zuko Godlimpi defended the move, framing it as essential for protecting local jobs and industry:

"It is not an affront on the relationship as such, but it is to tactically defend your employment capability in South Africa and the capacity of your industry to weather the storms."

Additionally, the government is proposing a 10% ad valorem customs duty on lithium-iron electric accumulators and considering anti-dumping duties to counter subsidized Chinese vehicle imports. These measures aim to strike a balance between keeping vehicles affordable for consumers and supporting domestic manufacturers.

WATCH: SA’s auto sector welcomes policy signals from SONA

Transition to Electric and New Energy Vehicles

South Africa’s automotive industry is undergoing a major shift toward electric and hydrogen-powered vehicles. With nearly half of the country’s vehicle exports going to the EU and UK – regions planning to phase out internal combustion engines by 2035 – local manufacturers are under pressure to adapt to maintain market access. In 2024, New Energy Vehicles (NEVs) made up only 3% of domestic sales, totaling 15,611 units. By October 2025, investments in NEVs had already surpassed R12 billion ($647 million).

In December 2023, the government unveiled the Electric Vehicles White Paper, outlining a roadmap for this transition. At the launch of the BMW X3 Plug-in Hybrid EV in July 2025, President Cyril Ramaphosa highlighted the potential of this shift:

"The global shift to clean vehicles is not just a challenge but an opportunity for South Africa to redefine its industrial future."

This transition is also driving the introduction of new tax policies designed to boost innovation and investment in the EV manufacturing sector.

Tax Incentives for EV Investments

The government has introduced tax incentives aimed at encouraging NEV production investments. These incentives are particularly beneficial for manufacturers who commit to building extensive NEV facilities. The Automotive Investment Scheme has allocated $39.3 million (R728.8 million) specifically for NEV-related projects, prioritizing genuine local production over simple assembly. Mikel Mabasa, CEO of NAAMSA, expressed optimism about these policies:

"With good government policies, we will attract new investment; we will increase and retain investment."

This momentum has already attracted interest from global automakers. For example, three Chinese automakers have entered non-disclosure agreements with NAAMSA to explore local assembly opportunities. Additionally, in February 2025, Mahindra South Africa signed a Memorandum of Understanding with the Industrial Development Corporation to study the feasibility of a Completely Knocked Down (CKD) vehicle assembly plant. This followed the milestone of assembling its 25,000th local "Pik Up" at its KwaZulu-Natal facility.

Using South Africa’s Mineral Reserves

South Africa’s wealth of mineral resources gives it a competitive edge in the global NEV market. As the world’s largest producer of platinum – a key component in hydrogen fuel cells – and a major supplier of manganese, nickel, lithium, and cobalt, the country is well-positioned to support lithium-ion battery production. To capitalize on this, the government has finalized the National Critical Minerals Strategy, which focuses on local processing of these resources for battery and fuel cell production. Parks Tau, Minister of Trade, Industry and Competition, described this as a pivotal moment:

"This is a once-in-a-generation opportunity to move beyond exporting raw materials and instead beneficiate locally, producing battery-grade inputs."

The strategy also includes plans to develop an "African Auto Pact" under the African Continental Free Trade Area. This initiative aims to align policies across the continent and establish a regional battery industry. In the interim, the government is considering reducing import duties on batteries to support the industry until a robust regional value chain is in place. The goal is to maximize the value derived from local production.

Comparison: SKD vs CKD Assembly Models

| Feature | SKD (Semi-Knocked Down) | CKD (Completely Knocked Down) |

|---|---|---|

| Local Content Levels | Low; involves assembling pre-painted bodies and major sub-assemblies | High; includes welding, painting, and sourcing significant local components |

| Job Creation | Limited; requires fewer workers | High; supports employment across manufacturing and supply chains |

| Investment Requirements | Lower; less complex machinery and smaller facilities needed | High; requires substantial capital for full-scale manufacturing plants |

| Policy Incentives | Minimal; often ineligible for full grants | Maximum; eligible for 150% tax deductions and Automotive Investment Scheme grants |

This comparison highlights the advantages of CKD assembly in meeting the Automotive Masterplan 2035’s targets for local content and job creation.

Growth Opportunities for the Industry

Partnerships with Chinese and Indian Manufacturers

South Africa’s automotive industry is making a notable shift from semi-knockdown (SKD) assembly to complete knockdown (CKD) production. This evolution is crucial, considering that 36% of imported vehicles come from India and 11% from China, while only 37% of vehicles sold locally are manufactured within South Africa. Transitioning these major importers into local manufacturers offers a chance to reshape the industry.

This process is already gaining momentum. Both Mahindra and Foton are progressing toward CKD operations, which create significantly more jobs compared to SKD assembly. For instance, in February 2025, Mahindra signed a memorandum of understanding with the Industrial Development Corporation to explore the feasibility of a CKD plant. This followed the assembly of its 25,000th Pik Up at its KwaZulu-Natal facility, with plans to launch the new plant between late 2026 and 2027. Similarly, Chinese manufacturer Foton announced in November 2025 its intention to join BAIC at the Coega Special Economic Zone to begin CKD production of the Foton Tunland bakkie. Parks Tau, South Africa’s Minister of Trade, Industry and Competition, highlighted the importance of this shift:

"The transition from SKD to CKD production marks a fundamental change in how vehicles will be made in South Africa… requiring deeper investment in local facilities, workforce skills and supply chains."

Further evidence of this trend can be seen in VSL Manufacturing’s $40.5 million (R750 million) investment in a component facility adjacent to the Isuzu plant in Gqeberha during 2025/2026. This demonstrates how localized manufacturing can attract upstream investments, bolstering South Africa’s position as a leading automotive hub on the continent.

Reclaiming Africa’s Manufacturing Hub Status

As of 2023, South Africa accounted for 54% of all vehicles assembled on the African continent. However, local content levels remain far below the 60% target outlined in the 2035 Masterplan. To reclaim its position as Africa’s manufacturing leader, South Africa must address the gap between imports and domestic production while leveraging opportunities presented by the African Continental Free Trade Area (AfCFTA).

The shift from SKD to CKD production is a critical part of this strategy. Strengthening local production and supply chains requires tightening policy loopholes that allow manufacturers to benefit from duty rebates without making meaningful local investments. Industry experts stress the importance of prioritizing genuine manufacturing efforts over basic assembly, with a focus on supplier development and localization.

A key area for improvement lies with Tier 2 and 3 suppliers, particularly in high-value sectors like electronics, powertrain, and telematics, where local contributions remain limited. Additionally, South Africa’s rich reserves of platinum and manganese position it as a natural partner for electric vehicle (EV) battery manufacturing. These resources could support the creation of circular value chains across the continent, further solidifying the country’s role in the global automotive landscape.

Policy incentives are instrumental in driving these changes, as shown in the table below.

Policy Incentives Comparison Table

| Incentive Program | Eligibility | Key Benefits | Timeline |

|---|---|---|---|

| APDP 2 (Production Incentive) | OEMs and Component Manufacturers (B-BBEE Level 4 required) | 50% duty rebate for vehicles; 62.5% for components/tooling | Effective until 2035 |

| NEV Tax Incentive | Manufacturers investing in NEV production facilities | 150% tax deduction on qualifying investment costs | Effective March 1, 2026 |

| Automotive Investment Scheme (AIS) | Light vehicle assemblers and component makers | 20% to 25% cash grant on plant and machinery investment | Ongoing; $39.3 million (R728.8 million) allocated for NEVs |

| VALA (Volume Assembly Localisation Allowance) | Light vehicle manufacturers with local value addition | Duty rebates to offset import duties on OEM components | 40% in 2021, decreasing to 35% by 2026 |

These programs are designed to prioritize genuine manufacturing efforts. By committing to CKD production with high local content, manufacturers can tap into multiple incentives, strengthening South Africa’s automotive sector and its broader economic impact.

Conclusion

South Africa’s auto assembly industry is at a turning point. Contributing 5.3% to the national GDP and supporting around 500,000 jobs across its value chain, the sector faces mounting challenges. These include competition from low-cost imports, reduced local content, aging infrastructure, and the global move away from combustion engines.

The situation is further complicated by export markets like the EU and UK – which account for nearly 50% of South Africa’s vehicle exports – planning to phase out fossil-fuel vehicles by 2035. As Parks Tau, Minister of Trade, Industry and Competition, cautioned:

"If we do not adapt, we risk losing these key export markets."

However, there are promising developments. A 150% tax deduction for qualifying investments in electric and hydrogen vehicles, starting March 1, 2026, has already encouraged big players like BMW and Ford to commit to producing plug-in hybrids locally.

The industry’s future hinges on bridging the gap between policy and execution. This means addressing SKD (semi-knocked-down) loopholes, strengthening Tier 2 and Tier 3 supplier networks, and tackling energy and logistics issues. A shift from SKD to CKD (completely knocked-down) manufacturing is particularly crucial. As Andrew Kirby, President and CEO of Toyota South Africa Motors, emphasized:

"SKD may be cheaper, but it is shallow. CKD is costly but transformative."

The direction is clear: bold, swift action will determine whether South Africa’s auto industry evolves or risks being left behind.

FAQs

How can South Africa stay competitive against low-cost vehicle imports?

South Africa can maintain its edge by boosting local manufacturing with targeted incentives, such as the Automotive Production and Development Program. This initiative encourages both investment and technological advancements. Aiming to raise local content to 60% by 2035 could fortify supply chains and cut down on dependency on imports. Shifting toward electric vehicle production, tackling infrastructure issues, and securing a reliable energy supply are also critical steps. These strategies not only attract investment but also help South Africa stay in sync with global market demands.

What needs to change for South Africa to build more EVs locally?

To ramp up local electric vehicle (EV) production in South Africa, several critical factors need attention: policy support, infrastructure upgrades, and investments in skills and technology. Expanding charging networks and ensuring a steady, reliable electricity supply are essential steps. Additionally, South Africa can tap into its rich reserves of platinum and nickel to support EV battery production.

Consumer incentives, like subsidies or tax rebates, could play a big role in encouraging EV adoption. Coupled with the current tax benefits for manufacturers, these measures could create a more favorable environment for both production and usage of EVs.

Why does moving from SKD to CKD matter for jobs and local content?

Shifting from SKD (Semi-Knocked Down) to CKD (Completely Knocked Down) manufacturing plays a key role in driving local industrial growth. CKD involves assembling vehicles using imported parts, which opens up opportunities for domestic component production. This shift not only creates more jobs but also helps develop a skilled workforce. Additionally, it strengthens supply chains and supports government efforts to boost local content, paving the way for a more competitive and self-reliant automotive sector.

Related Blog Posts

- Export Tax Incentives: Boosting SA Auto Exports

- Volkswagen’s African expansion starts in Kenya: what it means for SA

- Tax Incentives for EV Manufacturing in South Africa

- Exchange Rate Challenges for SA Car Makers

{kind=link}